Signature theoretic hedging of exotic derivatives under a personalized risk profile

Hedging a portfolio of arbitrary, path-dependent derivatives under a risk profile chosen by the user. A Python core plus an interactive web demo, built on the signature methods of Lyons et al. (2019).

The problem with exotic derivatives

Many derivatives have simple rules. A call option pays the asset's price at maturity minus a fixed strike. But as a contract's rules get more exotic, the mathematics needed to analyze it tends to get out of hand, and each new payoff often seems to need its own bespoke treatment. The effect is that the tractable contracts end up well understood while the interesting ones do not.

This project hedges derivatives whose payoff is a continuous function of the asset's price path, rather than only its final value. For example, a call option reads a single number off the path (its endpoint), while a variance swap reads how much the price moved over the window, regardless of where it ended up. The two contracts have little in common, yet both are continuous functions of the same path, and that is the only property this method needs.

What's more, the underlying theory conveniently lets you optimize for an arbitrary attitude toward risk. Much of the portfolio-hedging literature descends from mean-variance hedging, pioneered more than sixty years ago ( it shows its age...) Mean-variance assumes a specific Marginal Utility (How much you care about each extra dollar of wealth), and thus penalizes upside and downside symmetrically: a surprise gain is treated as exactly as regrettable as an equal surprise loss. Real traders are not so even-handed.

Here, a trader who fears losses more than they enjoy gains, or who has some situational need to shape a particular higher-order feature of the return distribution, can hedge directly under that preference. The demo takes this preference as an input and shows the resulting hedge side by side with the mean-variance answer, so you can watch the difference.

Signature theory

The basis is signature theory. A signature is a representation of a path that decomposes it into atomic patterns (arranged in complexity levels), and weights each with a coefficient. To achieve a hedge from this representation:

Take the asset's price path and enrich it slightly: add a temporal dimension, and a "lead-lag" copy of the path against itself (This is a standard trick that makes volatility visible to the integrals below). The levels are summarized as follows:

- Level 1 records the net change in each channel (where the path ended up).

- Level 2 records signed areas (how pairs of assets happen to co-move over time). This captures order and interaction that a net change throws away (it is, for instance, how realized variance becomes legible).

- Level 3 records a still finer interaction, and so on up.

Truncate at some level (they get progressively less influential, so this is usually defensible) and you have a finite feature vector that summarizes the entire path.

There's a very convenient property that makes all of this useful: any continuous function of the path can be written, to arbitrary accuracy, as a plain linear combination of signature terms. A nonlinear, history-dependent quantity can be written as one linear function. The signature linearizes the space of everything you might want to compute from a path.

Why this works in hedging

Two consequences follow:

First, a trading strategy is itself one of those functions. At each time t < T, how much of an asset you hold can depend on the entire path so far. So a strategy is just a linear readout of the running signature S_{0,t}: pick a list of coefficients ℓ, and your holding at time t is the inner product ⟨ℓ, S_{0,t}⟩. The same coefficients, evaluated as the path unfolds, generate the whole time series of holdings.

Secondly, the product of two signature-linear functions is again signature-linear (via an operation called the shuffle product). Follow the chain: your loss L at maturity is linear in the signature; your risk penalty P(L) (the polynomial encoding how much you dislike a loss of each size) is a polynomial in L, and so, after shuffling, still linear in the signature. Its expectation therefore collapses to a single inner product:

E[ P(L) ] = ⟨ P^shuffle(ℓ), E[S] ⟩

where E[S] is the expected signature of the asset's price path. You get E[S] from whatever describes the price dynamics: GBM, stochastic-volatility Heston, or anything you can simulate (closed-form for some models, Monte Carlo otherwise). Everything downstream is model-agnostic algebra.

So the problem "minimize my expected risk penalty over all possible feedback strategies" becomes "minimize one inner product over the coefficients ℓ, against a fixed vector E[S]." This is a finite, well-posed optimization. That is the trick the whole project rests on.

Dealing with Polynomials

The signature methods require a polynomial to properly weight the objective and optimize the hedge. Marginal utility is Taylor-decomposed into this polynomial, but unlike the simple Mean-Variance case, the resulting loss surface is nonconvex and requires numerical optimization techniques. Fortunately, the resulting polynomials can (like the signature itself) usually be truncated to a low degree. I use Homotopy Continuation, a tool from algebraic geometry that finds global optima by enumerating and checking solutions, which is fast as long as the polynomial degree (and thus solution count) is low.

The demo

The live demo lets you turn the knobs:

- pick a model of the underlying process — GBM or stochastic-volatility Heston;

- pick a contract — forward, Asian (average-price), or variance swap;

- dial your risk profile — the loss polynomial, i.e. how steeply you punish particular kinds of losses.

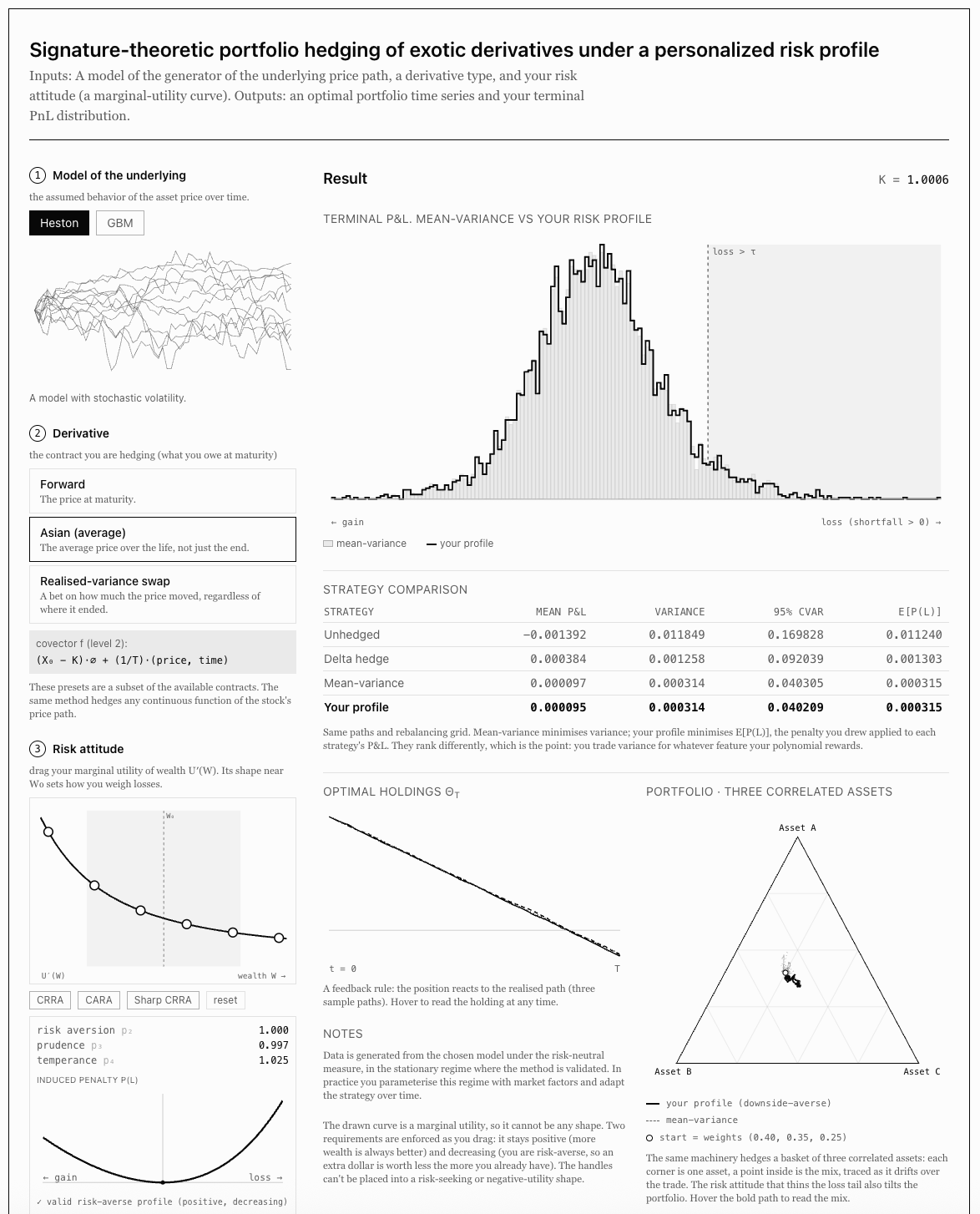

It then derives the optimal hedge, plots the resulting distribution of profit and loss, and overlays what plain mean-variance hedging would have done instead. Drag the risk sliders and watch the loss tail retreat. (It also traces the optimal allocation of a three-asset basket on a simplex, for the multi-asset case.)

Results

Benchmarked against a standard delta hedge and an unhedged position, on identical Monte Carlo paths and the same rebalancing grid (stable to within ~1% across seeds).

- Stochastic-vol (Heston) Asian. The signature hedge cuts variance ~75% and 95% CVaR (tail loss) ~57% versus the delta hedge, and ~97% / ~77% versus unhedged. GBM Asian is similar: ~75% variance and ~41% CVaR versus delta.

- Variance swap (Heston). Delta hedging is counterproductive here: it raises variance ~74% over not hedging at all, since a variance swap is a vega instrument with little first-order spot exposure. The signature hedge instead cuts variance ~57% versus the delta hedge.

- Forward (complete market). The signature hedge recovers the exact delta hedge, driving residual variance to ~0. A control confirming the method returns the known answer where one exists.

The risk profile is fit by homotopy continuation from the mean-variance solution, so it extends past the convex penalties of classical mean-variance hedging to arbitrary non-convex preferences, reaching hedges those penalties cannot.